Contents

- 1 Introduction: The Retirement Account Confusion That Costs You Money

- 2 The Core Difference: When You Pay Taxes (Now vs. Later)

- 3 The One Thing That Matters

- 4 Roth IRA vs. 401(k): Key Differences at a Glance

- 5 Roth IRA vs. Traditional 401(k) Comparison Table (2026)

- 6 The Big Takeaways

- 7 Compound Interest Hack: The Employer Match Is Free Money

- 8 Why You Should Never Skip Your 401(k) Match

- 9 When to Choose Roth IRA (The Tax-Free Growth Strategy)

- 10 Best for These People

- 11 Why Young People Should Love Roth IRA

- 12 The Withdrawal Flexibility Hack

- 13 When to Choose 401(k) (The High-Limit Strategy)

- 14 Best for These People

- 15 Why High Earners Should Choose 401(k)

- 16 The RMD Danger (Why 401(k) Can Be Risky)

- 17 The Roth 401(k): The Hybrid Option Most People Miss

- 18 What Is a Roth 401(k)?

Introduction: The Retirement Account Confusion That Costs You Money

Let me tell you about my friend Lisa. She’s 32, works at a tech company, and just got her first job offer with a 401(k). Her HR rep said: “You should contribute to your 401(k). It’s tax-advantaged.”

Lisa nodded, confused. But she also had a Roth IRA open from five years ago. She was told: “Roth IRA is better because it’s tax-free forever.”

So here’s Lisa, stuck between two choices, wondering: “Which one should I actually use? Can I use both? What if I pick the wrong one?”

If you’re feeling this same confusion, you’re not alone. Roth IRA vs. 401(k) is the most common retirement question Americans ask. And the wrong choice can cost you tens of thousands of dollars in taxes.

In this article, I’ll break down everything you need to know in plain English:

-

What’s the real difference between Roth IRA and 401(k)

-

2026 contribution limits (they changed!)

-

When to choose Roth IRA vs. traditional 401(k)

-

The employer match hack most people miss

-

Whether you can use both accounts together

-

A simple decision guide for your situation

Let’s get your retirement strategy figured out.

The Core Difference: When You Pay Taxes (Now vs. Later)

The One Thing That Matters

Here’s the secret most finance articles don’t tell you: The only difference between Roth IRA and 401(k) is when you pay taxes.

With a traditional 401(k): You get a tax break today. Your $10,000 contribution reduces your taxable income. But when you withdraw in retirement, you pay income tax on everything.

With a Roth IRA: You pay taxes on that $10,000 today. But every dollar your money grows into—$50,000, $100,000, $1 million—is 100% tax-free forever.

Simple analogy: Traditional 401(k) = “Pay later.” Roth IRA = “Pay now, never again.”

This is the foundation. Everything else is just details.

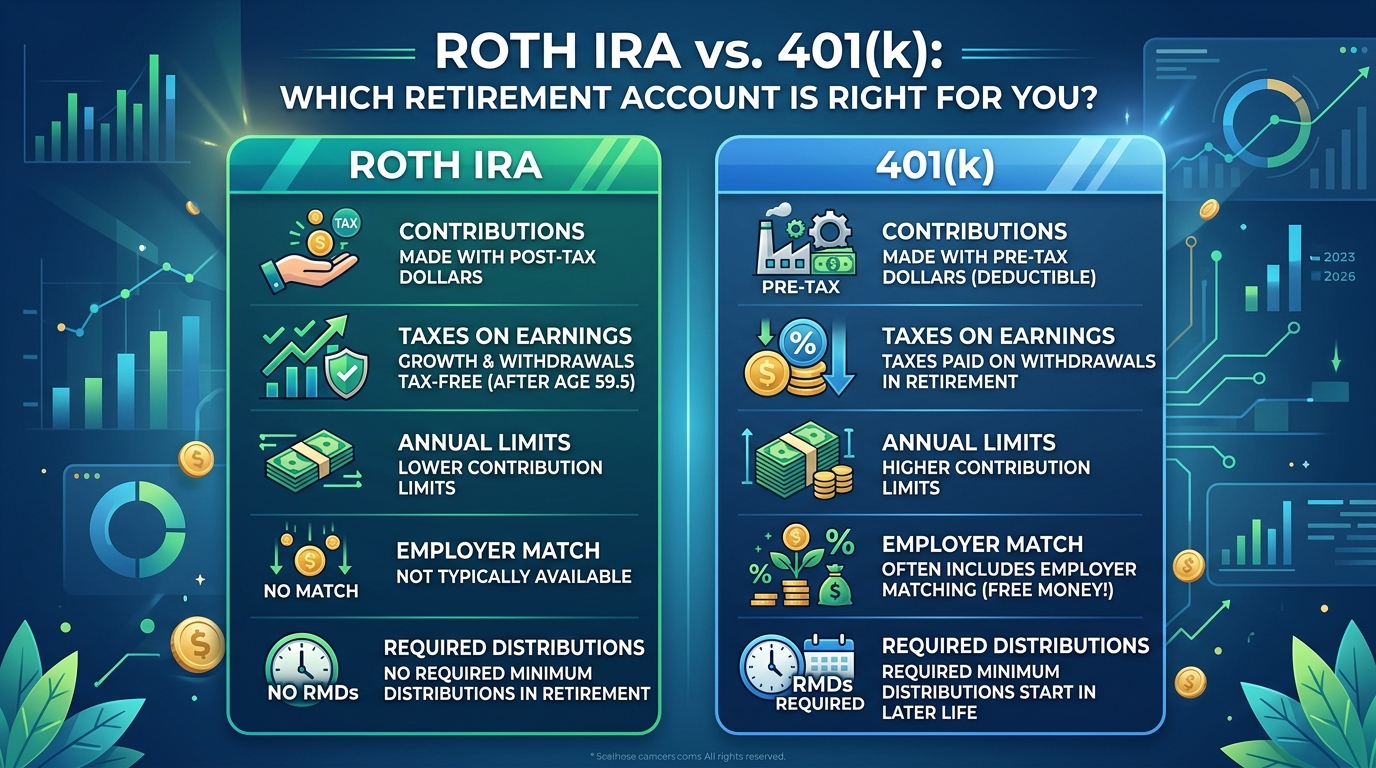

Roth IRA vs. 401(k): Key Differences at a Glance

Let’s compare the nuts and bolts. Here’s everything you need to know:

Roth IRA vs. Traditional 401(k) Comparison Table (2026)

The Big Takeaways

-

401(k) lets you save 3x more ($24,500 vs. $7,500)

-

Roth IRA has no RMDs (you don’t have to withdraw)

-

401(k) has employer match (this is FREE MONEY)

-

Roth IRA has income limits (high earners can’t contribute directly)

-

Roth IRA has more investment freedom (you choose everything)

Compound Interest Hack: The Employer Match Is Free Money

Why You Should Never Skip Your 401(k) Match

This is the most important tip in this article: If your employer offers a 401(k) match, you MUST contribute to get it.

Here’s how it works:

Lisa’s company offers 50% up to 6%. Her salary is $100,000. If she contributes 6% ($6,000), her employer adds $3,000. That’s an instant 50% return on her money. No stock picking. No risk. Just free money.

Rule: Always contribute at least enough to get the full employer match. It’s the closest thing to free money in investing.

This is the #1 reason to choose 401(k) over Roth IRA. You can’t get an employer match with a Roth IRA.

When to Choose Roth IRA (The Tax-Free Growth Strategy)

Best for These People

Choose a Roth IRA if:

✅ You’re younger than 40 (tax-free growth for 40+ years)

✅ Your income is below the limit (under $153K single, $242K married)

✅ You expect taxes to go up (Roth locks in today’s rates)

✅ You want flexibility (withdraw contributions anytime)

✅ You hate RMDs (no forced withdrawals after 73)

Why Young People Should Love Roth IRA

Let’s say you’re 25, earning $60,000. You contribute $7,500 to a Roth IRA. Your money grows at 8% annually.

After 40 years (age 65):

-

Traditional 401(k): $207,000 → Pay 22% tax → $161,000

-

Roth IRA: $207,000 → $207,000 tax-free

You get $46,000 more with Roth. That’s the power of tax-free growth for 40 years.

The Withdrawal Flexibility Hack

With a Roth IRA, you can withdraw your contributions anytime, tax and penalty-free. You can’t touch the earnings until 59½, but the money you put in? Gone. No problem.

This is perfect if you’re saving for:

-

A house (pull contributions for deposit)

-

Emergency fund (use Roth as backup)

-

Education (qualified withdrawals allowed)

Pro tip: Roth IRA is more flexible than 401(k). You own it, not your employer.

When to Choose 401(k) (The High-Limit Strategy)

Best for These People

Choose a traditional 401(k) if:

✅ You want to save more ($24,500 vs. $7,500 limit)

✅ Your employer offers a match (free money)

✅ You’re in a high tax bracket now (get bigger deduction)

✅ You expect lower taxes in retirement (pay less later)

✅ You’re age 50+ (catch-up is $8,000 vs. $1,100)

Why High Earners Should Choose 401(k)

Let’s say you’re 45, earning $250,000. You’re in the 35% tax bracket. You contribute $24,500 to a 401(k).

Tax deduction today: $24,500 × 35% = $8,575 saved on taxes

That’s like getting an instant 35% return on your contribution. With a Roth IRA, you pay taxes now, so you get no deduction.

The RMD Danger (Why 401(k) Can Be Risky)

After age 73, 401(k) forces you to withdraw money (Required Minimum Distributions). This can:

-

Increase your taxable income

-

Raise Medicare premiums (IRMAA)

-

Make your Social Security taxable

Roth IRA has no RMDs. You can let it grow forever.

Warning: Many retirees build huge 401(k) balances, then discover RMDs create a “tax trap” in retirement.

The Roth 401(k): The Hybrid Option Most People Miss

What Is a Roth 401(k)?

Some employers offer a Roth 401(k)—a hybrid that combines both accounts.

Why it’s great:

-

You get the high limit of 401(k) ($24,500)

-

You get tax-free growth like Roth IRA

-

No income limits (high earners can use it)

-

No RMDs (since January 1, 2024)

The catch: Your employer match still goes to a traditional 401(k), not Roth. So you’ll have two accounts: Roth 401(k) for your contributions, traditional 401(k) for the match.